Do you constantly live paycheck to paycheck? Do you always find it hard to save money? Join these money-saving challenges today. You’ll see how you can turn the seemingly daunting task of saving money into an exciting and achievable adventure.

To manage our money better, saving is one of the very first steps to take. Without saving a portion of our income, it would be difficult or even impossible to take control of our finances and achieve our financial goals. These goals include paying off debts, investing, allocating funds for emergencies, and planning retirement.

If you’re always struggling to save money, or if you find it hard to save constantly, or if you’re finding ways to save more and faster, embarking on a money-saving challenge can be an effective method.

Table of Contents

- 30-Day Money Saving Challenge

- Getting Started

- Save More Easily with Fun 30-Day Money-Saving Challenges

- Conclusion

30-Day Money Saving Challenge

You may start by participating in a 30-day challenge. It offers several advantages that make it an ideal starting point for individuals seeking to improve their financial habits:

- The shorter duration provides a sense of attainability and urgency, making it easier to commit to the challenge.

- The 30-day timeframe strikes a balance between immediate results and sustainability, allowing participants to witness tangible progress without feeling overwhelmed.

- It introduces the concept of discipline and financial consciousness in a manageable and engaging manner.

- The relatively shorter commitment minimizes the risk of burnout or losing interest, enhancing the likelihood of successfully completing the challenge.

- The challenge turns the seemingly daunting task of saving money into an exciting and achievable adventure.

Getting Started

1. Set Clear Goals for the Challenge

Before diving into the challenge, it’s essential to establish clear and achievable goals. Determine why you want to participate and what you intend to achieve by the end of the 30 days.

Whether you’re saving up for an emergency fund, a vacation, or paying off debt, having a specific goal will motivate you to stay on track.

2. Create a Budget for the Month

Crafting a budget is the cornerstone of successful money management.

Calculate your monthly income and allocate it across different categories, including essential expenses, discretionary spending, and savings.

Having a detailed budget in place will help you identify areas where you can cut back and allocate more funds toward your savings goal.

Whether you’re new to budgeting or wish to simplify your budgeting process, feel free to download our FREE monthly budget planner PDF.

3. Identify Areas of Potential Savings

Examine your spending habits and identify areas where you can make adjustments. This could include reducing dining out, curbing impulse purchases, or renegotiating subscription services. Even small changes in these areas can have a significant impact on your overall savings.

If you need more money-saving ideas, check out these 15 frugal habits of debt-free people.

Save More Easily with Fun 30-Day Money-Saving Challenges

1. The Incremental Savings Approach

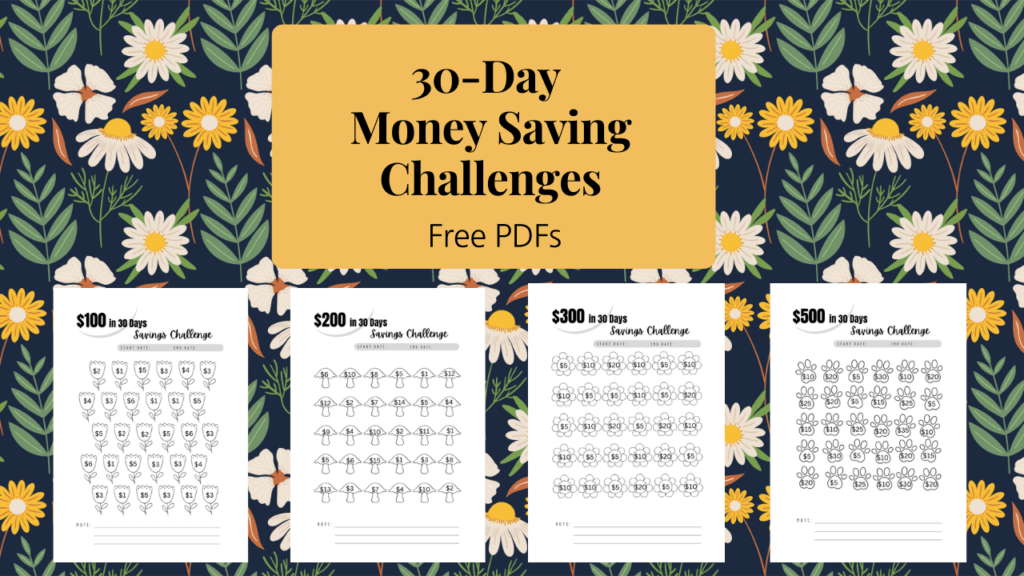

Start with our 30-day money-saving challenges, which are tailored to various savings goals.

Get Started Today!

Download and print out our 30-day money-saving challenge PDFs for FREE.

Depending on your income level and savings goal, choose whether you want to save $100, $200, $300, or even $500 in 30 days. Each day, you’ll contribute a specific amount to your savings and color your way to building your financial cushion.

Congratulate yourself when you successfully complete the challenge at the end of the 30 days. Feel free to celebrate this milestone and reward yourself.

However, don’t stop there. It takes time to build any new habit. Contrary to the myth that it takes only 21 days to develop a new habit, it’s probably more time-consuming than we thought.

So after completing your first money-saving challenge, repeat it once more or level up by challenging yourself to save a bigger amount in the next 30 days.

2. Level Up with 26-Week Challenges

After you successfully conquer the 30-day money-saving challenge 2 or 3 times, take yourself to the next level.

Our 26-week challenges are the perfect fit for those seeking a more substantial savings boost. These challenges span over half a year and you may choose from the challenges of saving $1,000, $3,000, or $5,000 in 26 weeks.

Level Up!

Get a collection of 9 fun challenges, a rainy-day fund page, and a customizable page to create a fund jar of your choice.

Extending the timeframe can create a sustainable and genuinely transformative savings habit.

3. Take It to the Next Level

If you’re committed to this challenge, the practice of saving money will gradually become easier and part of your daily routine.

Then it’s time to take part in a “Buy Essentials Only” challenge or a “No Spend” challenge.

The former requires you to commit to purchasing only the necessities for 30 days; while the latter involves cutting out all non-essential spending for a month.

These challenges will not only skyrocket your savings but also provide insight into what you truly need versus what you simply want.

4. Create Rainy Days Fund and Other Funds

In addition to these challenges, I also encourage you to consider allocating some of your savings toward specific funds.

A rainy day fund, for instance, can serve as a safety net during unexpected financial emergencies.

You can also create funds for future goals, such as a travel fund, a home renovation fund, or a retirement fund. By giving each fund a purpose, you’ll have a clear destination for your savings.

Conclusion

Money-saving challenges are a fun and exciting way to kickstart your new journey toward financial stability.

By setting clear goals, crafting a budget, and participating in various challenges, you’ll not only amass savings but also develop a healthier relationship with money.

The journey to financial freedom begins with a single step – are you ready to take it?

Have you tried any money-saving challenges? How has it changed your money habits? I encourage you to share your thoughts and experiences in the comments below. Your insights could inspire others who are on a similar journey toward financial fitness.

Save for later ⤵️